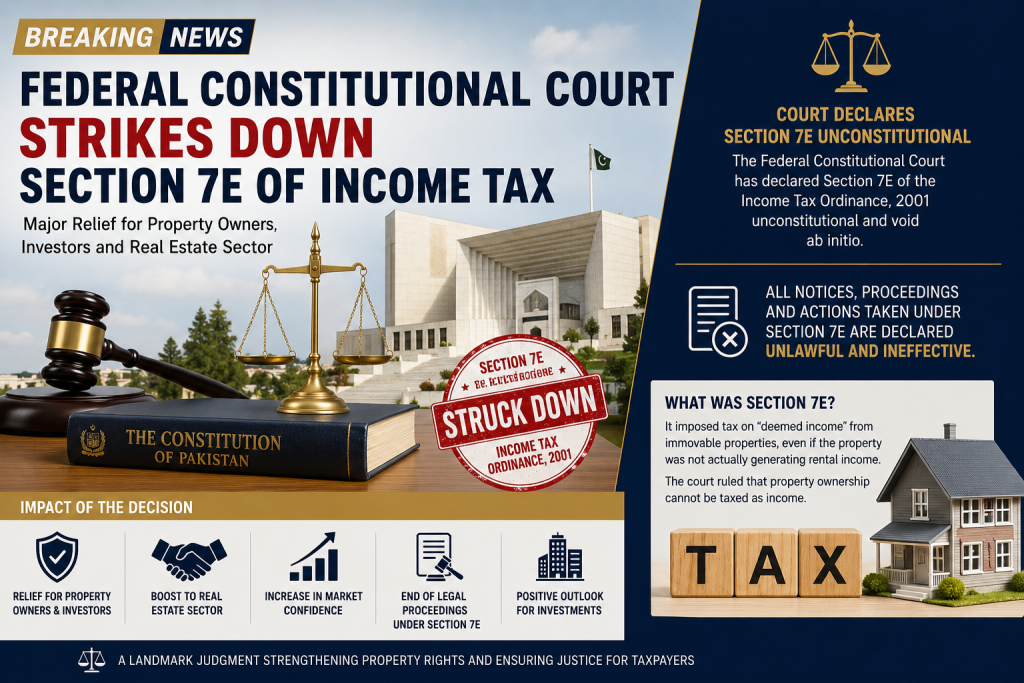

Federal Constitutional Court Strikes Down Section 7E of Income Tax Ordinance

Major Relief for Pakistan’s Property Industry

This groundbreaking judgment, which has profound effects on Pakistan’s property market as well as its tax system has struck down Section 7E of the Income Tax Ordinance, 2001, as unconstitutional. This judgment is being seen as one of the most significant ones from a judicial standpoint in recent years as far as Pakistan’s real estate industry is concerned.

Another important aspect of the judgment is that any proceedings that have been issued by the FBR in pursuance of Section 7E shall be rendered void and illegal. The impact of this verdict has been positive for the property industry of Pakistan as a whole.

What Was Section 7E?

The Section 7E came into effect by the Finance Act 2022 as a means of the government’s attempt to increase its revenue collection and widen the tax base. This tax law levied a tax on "deemed income" from immovable properties even if the property owner was not deriving rental income from his/her property.

According to this act,

Some immovable properties were assumed to be earning rental income automatically

The tax was to be paid on the basis of FBR’s assessment of the property value

The tax primarily affected the properties that were either unused or not rented out

Only one self occupied property could escape the tax

This tax law in essence imposed an annual tax on ownership of some properties irrespective of their income generation capacity.

Why Section 7E Was Controversial

From day one, Section 7E received criticisms from:

Property holders

Real estate developers

Tax authorities

Businessmen

Lawyers

These were justified criticisms because according to the opponents:

The government had no right to tax imaginary income

Owning property is not considered income at all

It was imposed upon the investors as an economic burden

It had negative repercussions on the real estate sector

Most stakeholders believed that the provision discouraged investment in property when the construction industry of Pakistan was already struggling.

The provision was also ambiguous in nature and the various High Courts offered conflicting rulings about its legal status.

Conflicting High Court Decisions

Section 7E was taken to several High Courts in Pakistan prior to its consideration by the Federal Constitutional Court.

The judgments varied from court to court:

The Peshawar High Court ruled it as unconstitutional

The Balochistan High Court also ruled it unconstitutional

The Islamabad High Court ruled some provisions of the act unconstitutional

The Sindh High Court ruled it as constitutional in certain circumstances

The Lahore High Court initially ruled it as constitutional but the position changed subsequently

Consequently, it was referred to the Federal Constitutional Court for its final determination.

Federal Constitutional Court Decision

The two judge bench, comprising Chief Justice Amin ud Din Khan and Justice Ali Baqar Najafi, disposed of the appeal petitions and passed the order which declared Section 7E as being unconstitutional.

This decision was based on the following points:

Section 7E is unconstitutional in its essence and substance

The provision represents a charge on the ownership of assets and is thus not an income tax

No parliament can levy such a tax according to the existing constitutional guidelines on income taxation

Additionally, the court opined that:

Section 7E will be deemed void ab initio

All pending notices and proceedings will be deemed terminated

Federal Board of Revenue's acts under Section 7E shall be considered null and void

Reasons for this judgment are expected to be given in detail soon.

Impact on Real Estate Sector

This decision will be highly favorable for the real estate industry in Pakistan.

According to real estate experts, this ruling is anticipated to:

Boost investor confidence

Help in property sales

Foster liquidity in the real estate market

Help reduce uncertainty from the market

Promote constructions

A number of investors had been holding off making any purchases due to fears over the tax implications of section 7E. This decision might promote more activities in:

DHA projects

Bahria Town

RUDA projects

Property markets

Investments in residential plots could also see increased interest.

There will certainly be a lot of benefits for the construction sector as well due to improved investor sentiments following this ruling.

Relief for Property Owners

Property owners from all over Pakistan consider this ruling a great blessing.

According to Section 7E,

- Owners of vacant land

- Non renting property investors

- Individuals owning more than one property

had been paying taxes annually without making any income from their properties.

Now that the provision has been made void,

- Pending notices can become null and void

- Ongoing lawsuits may be withdrawn

- Taxation in the future by using Section 7E will cease

This verdict particularly helped:

- Investors with long term investments

- Overseas Pakistanis

- Builders/developers

- Commercial investors

Impact on the Market

The real estate market responded well to the judgment.

Several property dealers and investors have indicated that the decision might:

- Surge the number of transactions

- Raise market confidence

- Moderate property prices

- Stimulate delayed investments

Some real estate analysts refer to the decision as the watershed moment for Pakistan’s troubled property market.

Conclusion

The judgment by the Federal Constitutional Court on Section 7E represents a groundbreaking event for Pakistan’s tax laws and real estate industry. This decision brings immediate benefits to property owners and investors and sets an important precedent for constitutional principles on taxing powers.

For the real estate industry, the decision is considered as an important positive indicator and may have a positive effect on investments in the near future.

With continuing evolution of Pakistan’s property market, the verdict in this case can be regarded as one of the key events of 2026.